Peak Oil Postponed… Once more: US EIA Worldwide Power Outlook

Visitor “divestment my @$$!” by David Middleton

Jude Clemente rocks!

Sep 29, 2019

The U.S. Division Of Power Says Extra Oil, Extra Pure Gasoline

Jude Clemente Contributor

Power

I cowl oil, gasoline, energy, LNG markets, linking to human improvement.

Quite a few power headlines from this previous week alone caught my consideration. They completely illustrate the huge scale of funding plans for oil and gasoline tasks around the globe. Listed below are only a few:

*”Japan to take a position $10 billion in world LNG infrastructure tasks.”

*”Tellurian Indicators $7.5 Billion LNG Pact With India’s Petronet.”

*”LNG investments hit report of $50 billion in 2019.”

*”Brazil’s Large $25 Billion Oil Public sale Clear Very Essential Hurdle.”

As destiny would have it, on Tuesday, a day after my birthday (I turned 25 once more), the U.S. Division of Power’s EIA launched its Worldwide Power Outlook 2019. It’s an excellent learn, and one which I deem obligatory for all Individuals, and even these globally fascinated by power. We must always all reap the benefits of the truth that we’ve got such authorities data freely obtainable to us open-source on-line.

It is best to know that the overwhelming majority of nations don’t have any such entry to their very own governments. Once more, that is the official modeling from the U.S. Division of Power and its Nationwide Power Modeling System. This isn’t from ExxonMobil, the Sierra Membership, or the American Wind Power Affiliation making an attempt to promote you one thing or make you assume a sure manner. That is the outlook of the U.S. Division of Power.

What’s previous is prologue: extra oil, extra pure gasoline. No kidding. These two important fuels provide almost 65% of the power used within the U.S. and world economies. International annual oil demand has been surging ~1.four million b/d since 2000 alone, with gasoline utilization up eight Bcf/d per 12 months.

[…]

The easy cause why we see such enormous investments in oil and gasoline as seen within the above headlines is as a result of we all know that the world will want much more of them. Particularly, the nonetheless growing world is wanting on the oil and gasoline consuming West to see how inexpensive and dependable power can develop economies and enhance human improvement.

[…]

The principle cause for the next graphic is that oil is the world’s most significant gas and has no important substitute in anyway. Oil is the foundation of globalization, utilized in virtually every part that we do, and essentially the most internationally traded commodity on this planet. Oil’s worth is so immense that too excessive of a value could cause a worldwide financial recession.

[…]

Subsequent comes the world’s go-to gas: pure gasoline.

Simply final 12 months alone, world gasoline demand jumped over 5% to a staggering 137 trillion cubic toes.

That’s a Marcellus’ shale price of manufacturing devoured each three weeks.

[…]

Forbes

Mr. Clemente’s graphs…

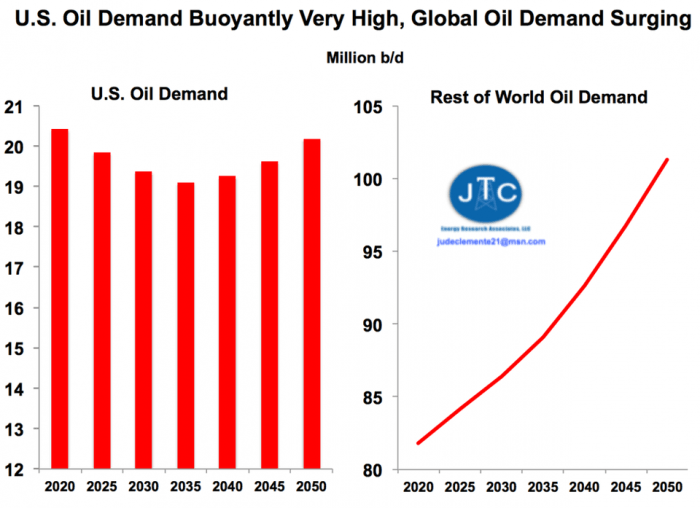

Determine 1. “U.S. oil demand will stay extraordinarily excessive, with world demand booming. DATA SOURCE: EIA’S IEO 2019; JTC”

Determine 1. “U.S. oil demand will stay extraordinarily excessive, with world demand booming. DATA SOURCE: EIA’S IEO 2019; JTC”

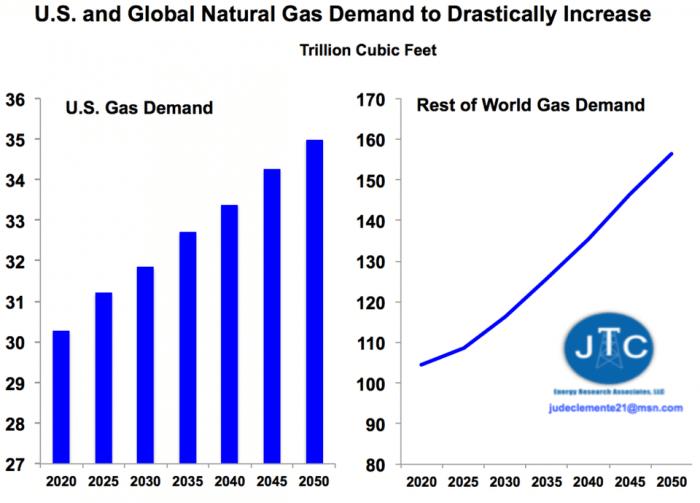

Determine 2. “The U.S. and the world are each in midst of a “sprint to gasoline” that may surge pure gasoline demand. DATA SOURCE: EIA’S IEO 2019; JTC”

Determine 2. “The U.S. and the world are each in midst of a “sprint to gasoline” that may surge pure gasoline demand. DATA SOURCE: EIA’S IEO 2019; JTC”

INTERNATIONAL ENERGY OUTLOOK 2019

Appears to be like like Peak Oil gained’t be getting right here earlier than 2050…

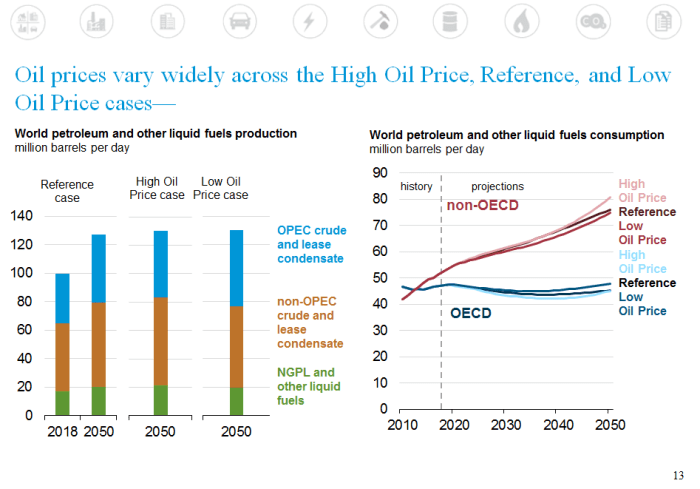

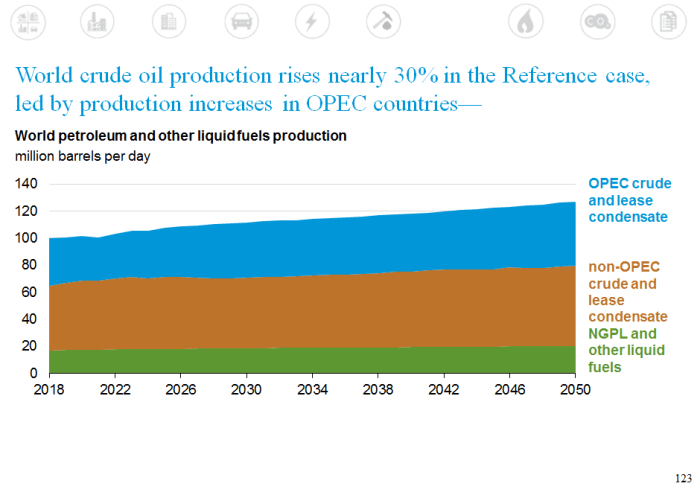

Determine three. Peak Oil Postponed… Once more. (US Power Data Administration)

Determine three. Peak Oil Postponed… Once more. (US Power Data Administration)

•Within the Reference case, world manufacturing of crude oil and lease condensate will increase from about 80 million barrels per day (b/d) in 2018 to 107 million b/d in 2050. Whole liquids manufacturing will increase from 100 million b/d in 2018 to 127 million b/d in 2050.

•Liquid fuels consumption will increase 45% in non-OECD nations and falls four% in OECD nations.

•Within the Excessive Oil Value case, world liquid fuels consumption in 2050 is four million b/d increased than within the Reference case. Primarily, rising, non-OECD nations drive sooner financial development, which contributes to increased power demand. Within the Excessive Oil Value case, proportionally increased quantities of crude oil are provided by nations that aren’t a part of the Group of the Petroleum Exporting Nations (OPEC).

•Within the Low Oil Value case, world liquids consumption in 2050 is 1 million b/d increased than within the Reference case. Slower non-OECD financial development assumptions result in decrease power demand, however the decrease costs imply that buyers use extra liquid fuels. Low-cost producers positioned in OPEC nations provide extra crude oil and condensate to the worldwide market.

US Power Data Administration

Too fracking humorous for phrases…

Determine four. Bwhahaha!!! (US Power Data Administration)

Determine four. Bwhahaha!!! (US Power Data Administration)

•Finish-use fuels embody these fuels consumed within the industrial, transportation, and buildings sectors and exclude fuels used for electrical energy technology.

•Liquid fuels, due to power density, price, and chemical properties, proceed to be the predominant transportation gas and an essential industrial feedstock.

•Electrical energy use within the residential and business constructing sectors will increase quickly due to rising revenue, a rising inhabitants, and elevated entry to electrical energy in non-OECD areas.

•Electrical energy use within the industrial sector and transportation sector additionally grows, respectively, because of rising product demand and rising use of electrical autos.

•Coal continues to be an essential end-use gas in industrial processes, together with the manufacturing of cement and metal.

US Power Data Administration

Right here’s the actually humorous bit…

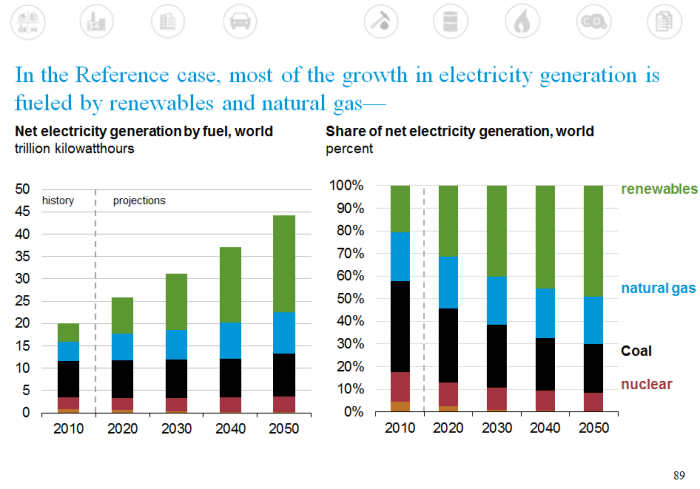

Determine 5. No power transitions right here. (US Power Data Administration)

Determine 5. No power transitions right here. (US Power Data Administration)

•Use of all major power sources grows all through the Reference case. Though renewable power is the world’s quickest rising type of power, fossil fuels to proceed to satisfy a lot of the world’s power demand.

•Pushed by electrical energy demand development and financial and coverage drivers, worldwide renewable power consumption will increase by three% per 12 months between 2018 and 2050. Nuclear consumption will increase by 1% per 12 months.

•As a share of major power consumption, petroleum and different liquids declines from 32% in 2018 to 27% in 2050. On an absolute foundation, liquids consumption will increase within the industrial, business, and transportation sectors and declines within the residential and electrical energy sectors.

•Pure gasoline is the world’s quickest rising fossil gas, rising by 1.1% per 12 months, in contrast with liquids’ zero.6% per 12 months development and coal’s zero.four% per 12 months development.

•Coal use is projected to say no till the 2030s as areas exchange coal with pure gasoline and renewables in electrical energy technology because of each price and coverage drivers. Within the 2040s, coal use will increase because of elevated industrial utilization and rising use in electrical energy technology in non-OECD Asia excluding China.

US Power Data Administration

Whereas EIA forecasts an explosive development in renewable power, it doesn’t exchange fossil fuels. It simply get piled on high of the power combine… Identical to fossil fuels and nuclear have been piled on high of biomass.

Determine 6. There has by no means been an power transition.

Determine 6. There has by no means been an power transition.

Extra excellent news…

Determine 7. No Inexperienced New Deal Cultural Revolution right here. (US Power Data Administration)

Determine 7. No Inexperienced New Deal Cultural Revolution right here. (US Power Data Administration)

Determine eight. Appears to be like like Ford F-Sequence pickup vans will nonetheless be outselling all EV’s in 2050. (US Power Data Administration)

Determine eight. Appears to be like like Ford F-Sequence pickup vans will nonetheless be outselling all EV’s in 2050. (US Power Data Administration)

Whereas they forecast that renewable power sources will account for almost half of world electrical energy technology by 2050, whole demand greater than doubles. The expansion in renewable power barely retains up with whole demand development.

Determine 9. Coal remains to be alive and properly in 2050. (US Power Data Administration)

Determine 9. Coal remains to be alive and properly in 2050. (US Power Data Administration)

Oops!

Determine 10. ROTFLMFAO!!!!!. (US Power Data Administration)

Determine 10. ROTFLMFAO!!!!!. (US Power Data Administration)

Did I point out that Peak Oil has been postponed… Once more?

Determine 11. Yi-hah!!!!! (US Power Data Administration)

Determine 11. Yi-hah!!!!! (US Power Data Administration)

Even higher information…

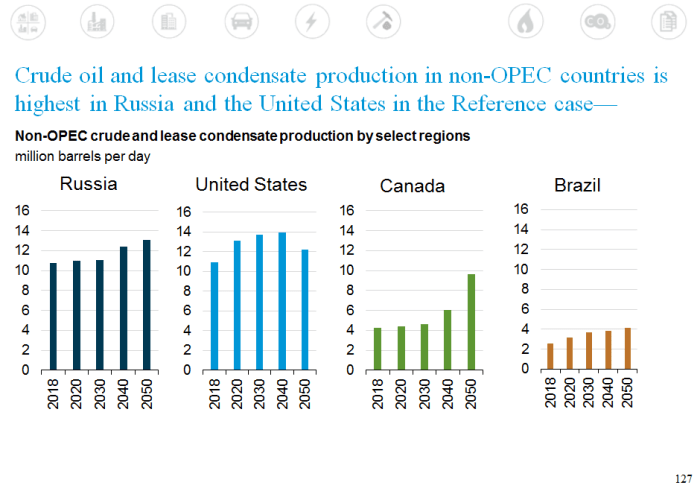

Determine 12. The US may hit the Hubbert peak by 2040… Nearly when Canada kicks it up a notch. (US Power Data Administration)

Determine 12. The US may hit the Hubbert peak by 2040… Nearly when Canada kicks it up a notch. (US Power Data Administration)

•Non-OPEC crude oil and lease condensate manufacturing grows 23% between 2018 and 2050, reaching 59 million b/d in 2050. These will increase are pushed by development in Russia (22%), america (11%), Canada (126%), and Brazil (59%).

•United States crude oil and lease condensate manufacturing will increase from 11 million b/d in 2018 to roughly 14 million b/d from 2025 to 2040, pushed by hydraulic fracturing of tight sources within the U.S. Southwest. Subsequent manufacturing falls to 12.2 million b/d by 2050, as improvement strikes into much less productive areas and properly productiveness declines. Nonetheless, 2050 manufacturing will increase 11% from 2018 ranges.

•Russia’s 2.three million b/d enhance in manufacturing by 2050 comes primarily from non-tight sources, however the nation additionally sees accelerated development in tight oil manufacturing after 2030.

•Canada’s 5.four million b/d enhance in manufacturing by 2050 is a results of oil sands improvement, notably towards the tip of the projection interval, as simply accessible world sources are more and more depleted and world oil costs step by step enhance.

•Brazil’s 1.5 million b/d enhance in manufacturing by 2050 outcomes from continued improvement of offshore pre-salt oil sources.

US Power Data Administration

Extra offshore drilling and oil sands improvement! Too fracking cool.

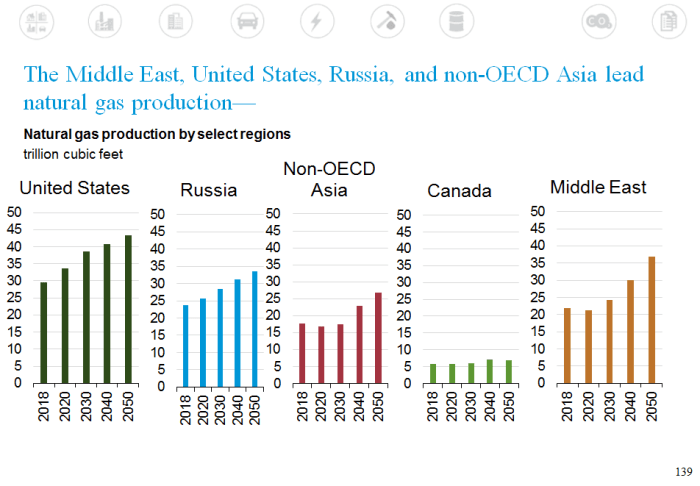

The US will proceed to kick @$$ in relation to pure gasoline…

Determine 13. No Hubbert Peaks in sight.. (US Power Data Administration)

Determine 13. No Hubbert Peaks in sight.. (US Power Data Administration)

And now for the pièce de résistance…

Determine 14. Did I already use the Dr. Evil chortle? (US Power Data Administration)

Determine 14. Did I already use the Dr. Evil chortle? (US Power Data Administration)

Might the EIA Projections Be Mistaken?

Positive they might. EIA completely missed the shale revolution.

Determine 15. EIA completely missed the shale revolution.

Determine 15. EIA completely missed the shale revolution.

Like this:

Loading…