2020’s Most and Least Financially Literate States

Monetary literacy is the power to grasp and use cash abilities to take care of your private funds. This principally applies to easy cash abilities the on a regular basis particular person makes use of, like constructing a grocery funds and saving for a wet day and retirement.

Our first experiences with cash sometimes start once we get our first allowance or money as a birthday present. Most of us in all probability relate to saving up from mowing lawns, or another easy enterprise, to purchase the latest online game. Then we head to the shop, seize the sport, and get to the checkout the place we study gross sales tax as a result of our precise quantity of $59.99 wasn’t sufficient.

Relying on what state you’re in, you in all probability realized a bit of extra about budgeting, taxes, and the way to decide on a bank card with a low APR in highschool economics or private finance. For a lot of others, your college could not have required and even supplied these alternatives, leaving you to Google “learn how to funds” to advance your monetary schooling by yourself.

Monetary literacy is the core of wholesome cash administration and a vibrant monetary future, and it begins with what you be taught as a baby and in class. This units the tone for a way you funds and save, which is why we got down to be taught which states are probably the most financially literate, and which have some studying to do.

We analyzed which states require financial and private finance schooling in highschool and in contrast median family revenue with common family debt to find out which states are probably the most financially literate.

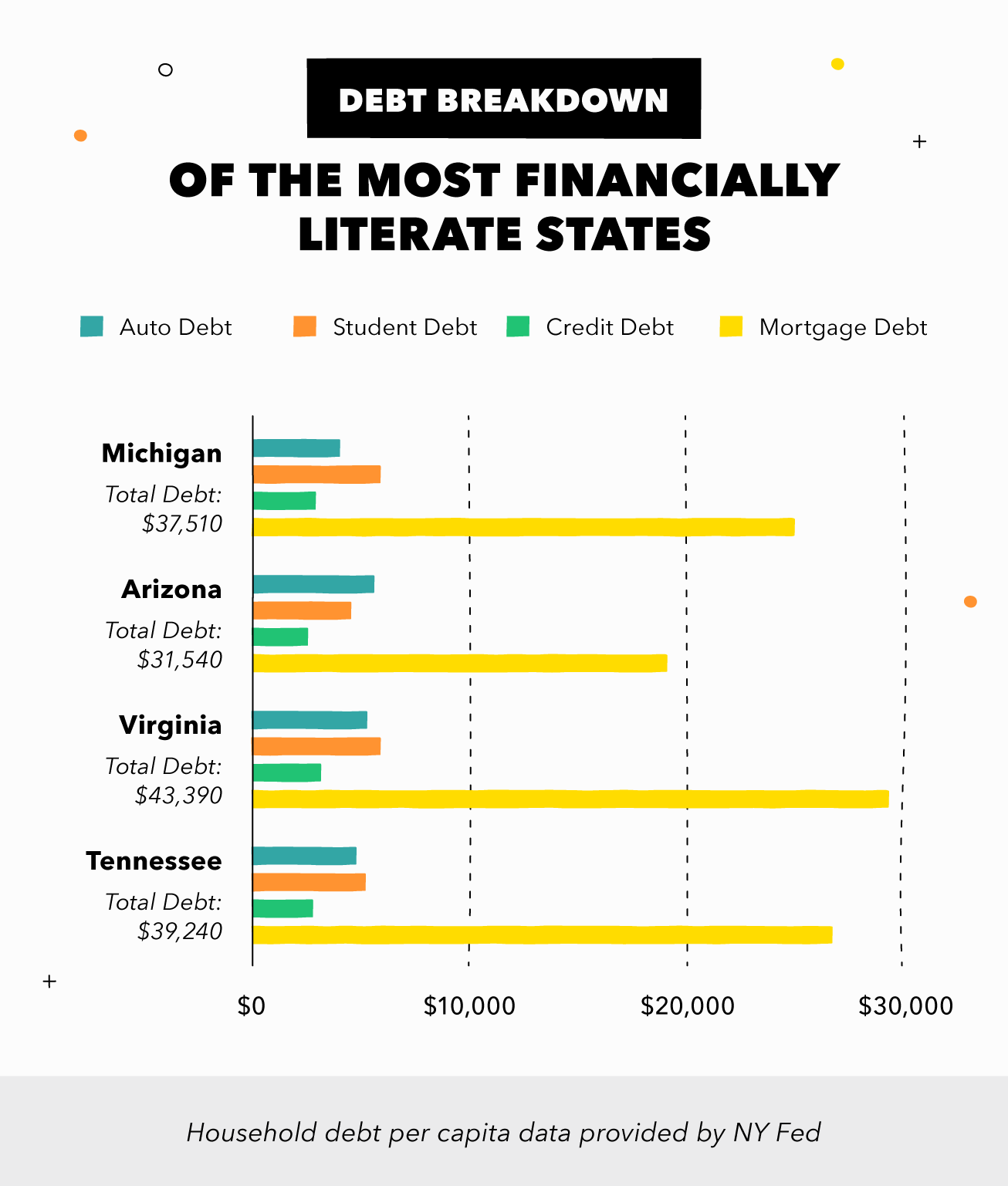

Most Financially Literate States

These states not solely worth monetary schooling greater than most, however additionally they have comparatively low ranges of debt in comparison with their median wage and revel in an general secure monetary well-being. Michigan, Arizona, Virginia, and Tennessee make the grade in the case of monetary literacy.

1. Michigan

Michigan has the second-highest monetary schooling necessities — providing each economics and private finance programs, in addition to testing college students on each topics. The Nice Lakes State additionally comes 13th for the bottom debt-to-income ratio with a mean family debt of $37,510 versus a median revenue of $56,697. Michigan has the very best monetary well-being rating of any state at 51, that means greater than half of residents have automated financial savings deposits and 32 p.c at all times repay their bank cards in full.

Monetary well-being rating of 51

Ranks 13th for debt-to-income ratio

Exams on economics and private finance

2. Arizona

Though Arizona beats out Michigan with the fourth-lowest debt-to-income ratio, the bottom of our checklist, there’s a massive hole within the state’s schooling necessities. Arizona requires each economics and private finance to be supplied however solely requires economics to be taken as a part of their core curriculum.

Monetary well-being rating of 49

Ranks 4th for debt-to-income ratio

Solely requires an economics course and no testing

three. Virginia

Virginia is called the birthplace of the nation and likewise takes the title of third most financially literate state. Virginia and Tennessee each supply and require private finance and economics programs be taken in highschool, however don’t embrace both of their standardized testing course of. Virginia additionally falls simply in need of Michigan with $17,262 extra common debt than they’re estimated to repay in a yr.

Monetary well-being rating of 49

Ranks 14th for debt-to-income ratio

Requires each private finance and economics programs, however no testing

four. Tennessee

Whereas Tennessee brings residence the 10th lowest wage within the U.S. the info present they handle their cash fairly properly. Regardless of making little greater than $52,000, they’ve the 19th lowest debt-to-income ratio with a mean $39,240 in debt. In addition they have a monetary well-being rating of 49, that means a majority of Tennesseeans have not less than a few hundred dollars in financial savings however they do discover it considerably troublesome to make ends meet.

Monetary well-being rating of 49

Ranks 19th for debt-to-income ratio

Requires each private finance and economics programs, however no testing

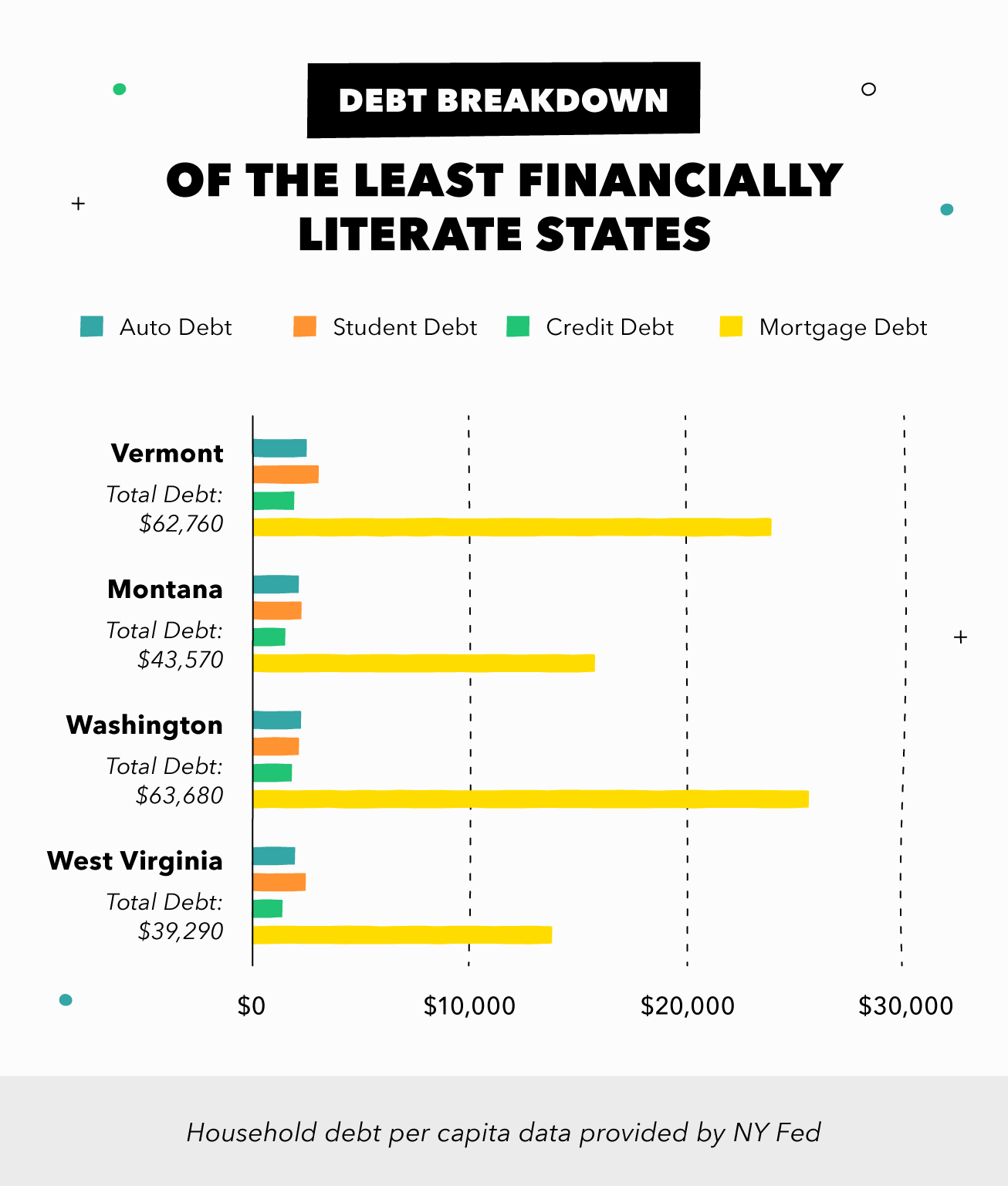

Least Financially Literate States

These 4 states not solely have decrease monetary schooling necessities than others however could have a more durable time paying their payments. They’re additionally extra more likely to have a disproportionate quantity of debt assuming they spend the really useful 36 p.c of their revenue paying off their loans and bank cards. Vermont, Montana, Washington, and West Virginia could have to hit the books to enhance their monetary literacy.

1. Vermont

Vermont comes final in our examine, with the fourth-highest debt ratio with $62,760 in debt, in comparison with their median family revenue of $60,782 with an anticipated yearly debt payoff of $21,882. Moreover, Vermont has no schooling necessities. In truth, excessive faculties aren’t required to supply economics or private finance programs in any respect.

Monetary well-being rating of 46

Ranks 47th for debt-to-income ratio

Programs aren’t required to be supplied

2. Montana

Montana is the one state in our backside 4 that has any highschool course expectations, although it solely requires that prime faculties supply a private finance course. The Treasure State additionally ranks 29th for debt-to-income ratio, with $23,652 of debt left after a yearly payoff of $19,917, primarily based on a median revenue of $55,326.

Monetary well-being rating of 47

Ranks 29th for debt-to-income ratio

Programs aren’t required to be supplied

three. Washington

Washington state has the fifth-highest debt per family within the U.S. and the very best at $63,680 of debt. Whereas additionally they make fairly a bit greater than many different states at $74,073 a yr, that’s not sufficient to save lots of them from having the 11th highest debt-to-income ratio of our examine — particularly when you think about that they haven’t any finance schooling necessities included into their curriculum.

Monetary well-being rating of 48

Ranks 42nd for debt-to-income ratio

Programs aren’t required to be supplied

four. West Virginia

West Virginia has the bottom median revenue of our checklist, incomes simply over $44,000 a yr. Their common debt isn’t too far behind, with $39,290 owed per family. That’s sufficient for them to tug simply forward of Montana for his or her debt-to-income ratio, rating 27th general. Nevertheless, they’re tied for the bottom monetary well-being rating at 46 and have zero monetary schooling necessities.

Monetary well-being rating of 46

Ranks 27th for debt-to-income ratio

Private finance have to be supplied

Monetary Schooling Assets

It’s by no means too late to be taught extra about cash! If you happen to’re able to level-up your monetary know-how, listed here are some assets for each age and skill stage.

Tricks to Train Children About Cash

The earlier we introduce the idea of cash, incomes, and monetary accountability to youngsters, the higher palms our nation’s monetary future will likely be in. A small allowance and apply saving is a superb place to begin, however don’t overlook to cowl the gross sales tax if you exit procuring. You may as well ditch the money and get your baby an allowance debit card. This manner you possibly can train them to trace their stability and apply fundamental math whereas studying about curiosity.

Cash issues are additionally straightforward to gamify. You’ll be able to apply counting cash for rewards, supply financial savings incentives like a pizza occasion so as to add “curiosity,” or apply planning and pitching enterprise concepts for a household sport evening. There are many child-friendly cash studying assets accessible.

The Greatest Finance Courses for Teenagers

As soon as we attain adolescence, cash classes develop into a bit of extra critical. Not solely as a result of teenagers have loads of alternatives to earn their very own revenue, however as a result of school, and the heavy tuition costs that go together with it, are simply across the nook. Analysis exhibits that younger adults who obtain monetary schooling are much less more likely to carry bank card debt, and extra more likely to apply to and obtain grants and monetary help.

Lower than 17 p.c of excessive schoolers are required to take monetary schooling programs, whereas 70 p.c of teenagers have entry to those programs. Encourage your teen to take any courses their college gives and work with them at residence to counterpoint their studying.

Youthful teenagers are doubtless enthusiastic about their driver’s license and part-time jobs, each of that are nice studying alternatives to make the most of. Whether or not your baby will likely be paying for his or her first automobile and insurance coverage or you can be, have them assist you construct a financial savings plan and funds for automobile upkeep and gasoline. If you happen to’ll be taking out an auto mortgage, have them take part on the method and assist calculate rates of interest and month-to-month funds.

For older teenagers, contemplate serving to them search for monetary help and select an emergency bank card. This can provide you peace of thoughts whereas additionally serving to them construct credit score. Be certain that they perceive annual charges, APR, and minimal funds. Then signal them up for a credit score monitoring app like Mint to allow them to see how making funds on time, lacking funds, and credit score inquiries can have an effect on their rating.

Monetary Duty for Adults

If you happen to really feel such as you’ve missed out on invaluable monetary info otherwise you’re wanting into your first massive buy, like a home or a automobile, then there are many assets on-line that can assist you study cash. Step one is deciding your lesson.

If you happen to’re seeking to construct a funds, you’ll wish to begin by understanding fundamental funds breakdowns. The preferred system is the 50/30/20 rule, which breaks down your month-to-month revenue into wants, needs, and financial savings. Record out all your purchases and divide them into these three classes, then determine the place it’s good to reduce on spending. Then construct a spreadsheet or obtain a budgeting app that can assist you keep on observe.

From there you possibly can observe monetary bloggers, YouTubers, and revered monetary personalities to remain up-to-date on common monetary developments. Your greatest wager is to check-in on issues it’s good to know as you want them. For instance, should you’re seeking to purchase a brand new residence, YouTube has hours of assets to assist stroll you thru the mortgage utility course of, learn how to save for a down fee, help applications, and the way a lot you must save for closing prices.

If you would like extra direct and strong studying, you possibly can at all times enroll in neighborhood school programs. Many will likely be accessible on-line so you possibly can match them into your schedule, and you may select subjects as broad or particular as you’d like. Many establishments additionally supply grants, monetary help, and fee choices that can assist you cowl the prices.

In fact, an authorized monetary planner is one of the best ways to get present and correct info. They’re an excellent useful resource for funding and financial savings methods and may construct a plan custom-made on your monetary wants.

Whereas monetary schooling varies throughout the nation, there are nonetheless loads of alternatives so that you can advance and share your cash information. From monitoring your credit score rating to studying learn how to make investments, there’s at all times room to level-up your monetary literacy.

Methodology

For this examine, we in contrast family revenue knowledge from the Census with family debt totals from the NY Fed to find out the quantity of debt households have in comparison with their annual estimated debt contributions utilizing the 28/36 rule.

We additionally examined the Council for Financial Schooling’s analysis on monetary literacy schooling and entry and the Shopper Monetary Safety Bureau’s monetary well-being rankings.

The info weights had been as adopted:

Monetary schooling programs supplied (pre-weighed by necessities) – 50%

Debt-to-income comparability – 30%

Monetary well-being score – 20%

Sources: Census | New York Fed | Shopper Monetary Safety Bureau | SoFi